My pick: Janus Enterprise Fund JAENX

Searching for Mid-Cap Growth funds with no load available through etrade, I take a look at the 18 funds with the best 3 year performance.

Then I cross out any fund with an expense ratio over 1.5% or a turnover rate of over 100%.

Then I note that 2 of the remaining 8 funds have lagged the group recently so I rule them out.

NBNGX has a $5000 minimum initial investment which is too high.

This leaves:

BARON ASSET (BARAX)

COLUMBIA ACORN SELECT Z (ACTWX)

JANUS ADVISER MID CAP GROWTH S (JGRTX)

JANUS ENTERPRISE (JAENX)

SELECTED SPECIAL SHARES S (SLSSX)

According to their Style Composition charts, BARAX and ACTWX are invested in many categories beyond Mid-Cap Growth with ACTWX investing heavily in Small-Cap Value

and BARAX with its largest position in Small Cap Growth.

None of the other three are completely focused on Mid-Cap Growth but they have solid Mid-Cap investments and are Growth focused. Any of these would make decent choices, but I am choosing the one with the lowest expenses- Janus Enterprise Fund JAENX

12.30.2006

Check you Credit Report for free

If you are a legal US resident, you are entitled to one free credit report every 12 months. December stirkes me as a good time to make sure my credit information is accurate.

If you search around for the site to check your credit report, you will find dozens of sites with similar names that will let you check your credit report. Many will force you to sign up for a service that is not free after one month to then lead you to your 'free' credit report. How this is legal is beyond me.

This site will allow you to check you credit reports with Equifax, TransUnion, and Experian, for FREE. Of course each of these companies will attempt to sell you things- like your credit score, and extra credit protection, etc- but you can view your reports, online for free, without paying a cent by declining the offers.

Here is the site:

https://www.annualcreditreport.com/cra/index.jsp

If you search around for the site to check your credit report, you will find dozens of sites with similar names that will let you check your credit report. Many will force you to sign up for a service that is not free after one month to then lead you to your 'free' credit report. How this is legal is beyond me.

This site will allow you to check you credit reports with Equifax, TransUnion, and Experian, for FREE. Of course each of these companies will attempt to sell you things- like your credit score, and extra credit protection, etc- but you can view your reports, online for free, without paying a cent by declining the offers.

Here is the site:

https://www.annualcreditreport.com/cra/index.jsp

12.28.2006

Is the US national debt a problem?

Beats me. I majored in Philosophy, not Economics. My expertise would be more on the question- what does it mean that the US has a lot of debt… or why does debt exist… or if debt goes up and no one is paying attention, does it make a sound? (apparently not!)

Regardless- here is one opinion that thinks the US will soon collapse under the weight of its massive debt.

Actually, Dr. Chris Martenson fears that the real result will be decrease in the standard of living and skyrocketing inflation as the US tries to print itself out of its debt.

And here is another opinion that suggests US debt is low, relatively speaking and that the debt doomsday crowd will worry itself to extinction. Actually Mike Norman references Alexander Hamilton and states "…having a national debt is a national treasure, because it's a reflection of a nation's ability to establish and maintain credit.”

The most telling thing to me, when reading these two opinions side by side, is which sets of numbers each chooses to focus on and how they do not match. Both articles are from 2006 but Dr. Martenson’s was written after a recent US financial report was released. This report starts by claiming that there are not sufficient financial controls in place to verify the accuracy of the data. Having studied human nature a bit. I take this to indicate that the debt is likely more than reported. I then listen to Mr. Norman and have to agree, when compared to other governments, ours grows and produces quite admirably.

Regardless- my take away from this is to recommit to a mission of diversifying while investing- large companies and small, US, international, developed and developing markets, short term debt (bonds) long term debt, real estate, etc. Money will flow from one trend to another and if you are invested broadly, with good analysts picking sound companies, and contributing diversely and consistently, you ought to be able to build some wealth.

Thanks to Dave for forwarding Dr. Martenson's article.

Regardless- here is one opinion that thinks the US will soon collapse under the weight of its massive debt.

Actually, Dr. Chris Martenson fears that the real result will be decrease in the standard of living and skyrocketing inflation as the US tries to print itself out of its debt.

And here is another opinion that suggests US debt is low, relatively speaking and that the debt doomsday crowd will worry itself to extinction. Actually Mike Norman references Alexander Hamilton and states "…having a national debt is a national treasure, because it's a reflection of a nation's ability to establish and maintain credit.”

The most telling thing to me, when reading these two opinions side by side, is which sets of numbers each chooses to focus on and how they do not match. Both articles are from 2006 but Dr. Martenson’s was written after a recent US financial report was released. This report starts by claiming that there are not sufficient financial controls in place to verify the accuracy of the data. Having studied human nature a bit. I take this to indicate that the debt is likely more than reported. I then listen to Mr. Norman and have to agree, when compared to other governments, ours grows and produces quite admirably.

Regardless- my take away from this is to recommit to a mission of diversifying while investing- large companies and small, US, international, developed and developing markets, short term debt (bonds) long term debt, real estate, etc. Money will flow from one trend to another and if you are invested broadly, with good analysts picking sound companies, and contributing diversely and consistently, you ought to be able to build some wealth.

Thanks to Dave for forwarding Dr. Martenson's article.

12.19.2006

Non-Ret: Foreign Sml/Mid Growth

My Pick: Columbia Acorn International Select Fund/Z ACFFX

Looking at International funds that invest in small or mid sized companies through Etrade's fund screener is not easy. They allow you to pick "Equity International Small Company " and "Equity Global Small Company" with the second category presumably also investing in US companies. I found however, that screening out al the global funds and then checking the category at Morningstar uncovered a few additional choices that were focused no smaller companies.

Columbia Acorn International Select Fund/Z ACFFX

Columbia Acorn International Fund/Z ACINX

Neuberger Berman International/Trust NBITX

All three have turnover ratios below 50% which is much lower than the 91.68% average listed for Small Company Foreign funds and the expenses are all less than the 1.67% average of the group.

NBITX has done well (I actually own it) but has lagged recently and has the highest turnover of the bunch. ACINX has the lowest expenses and has done almost as well as ACFFX- it has likely beaten ACFFX when you take the expenses into account. But I am picking ACFFX for our hypothetical portfolio.

Why? you might ask...

ACINX has $3,713.67 million under management

ACFFX has $121.01 million under management

As of 10/13/06 ACINX had 1.45 % of its assets in its largest holding: Hexagon, a Swedish Industrial Materials company (according to Morningstar). 12.09% of its assets are in its top ten holdings.

As of 10/13/06 ACFFX had 5.73 % of its assets in its largest holding C&C Grp, an Irish Consumer goods company (Morningstar). 36.41% of its assets are in its top ten holdings.

Funds that invest in small companies have to be concerned about what their purchase or sale of stock in a company will do to the price of that company's stock since smaller companies do not have as many shares outstanding and do not trade at the same high volumes as large companies. If a fund manager attempts to buy or sell a $200 million stake in a company that only has $2 billion worth of stock outstanding- that action may have an impact on the price she will be able to get for her transaction.

So my belief is that ACFFX will be able to make adjustments easier and focus on a smaller number of companies which will hopefully be more efficient in the long run.

Looking at International funds that invest in small or mid sized companies through Etrade's fund screener is not easy. They allow you to pick "Equity International Small Company " and "Equity Global Small Company" with the second category presumably also investing in US companies. I found however, that screening out al the global funds and then checking the category at Morningstar uncovered a few additional choices that were focused no smaller companies.

Columbia Acorn International Select Fund/Z ACFFX

Columbia Acorn International Fund/Z ACINX

Neuberger Berman International/Trust NBITX

All three have turnover ratios below 50% which is much lower than the 91.68% average listed for Small Company Foreign funds and the expenses are all less than the 1.67% average of the group.

NBITX has done well (I actually own it) but has lagged recently and has the highest turnover of the bunch. ACINX has the lowest expenses and has done almost as well as ACFFX- it has likely beaten ACFFX when you take the expenses into account. But I am picking ACFFX for our hypothetical portfolio.

Why? you might ask...

ACINX has $3,713.67 million under management

ACFFX has $121.01 million under management

As of 10/13/06 ACINX had 1.45 % of its assets in its largest holding: Hexagon, a Swedish Industrial Materials company (according to Morningstar). 12.09% of its assets are in its top ten holdings.

As of 10/13/06 ACFFX had 5.73 % of its assets in its largest holding C&C Grp, an Irish Consumer goods company (Morningstar). 36.41% of its assets are in its top ten holdings.

Funds that invest in small companies have to be concerned about what their purchase or sale of stock in a company will do to the price of that company's stock since smaller companies do not have as many shares outstanding and do not trade at the same high volumes as large companies. If a fund manager attempts to buy or sell a $200 million stake in a company that only has $2 billion worth of stock outstanding- that action may have an impact on the price she will be able to get for her transaction.

So my belief is that ACFFX will be able to make adjustments easier and focus on a smaller number of companies which will hopefully be more efficient in the long run.

12.13.2006

How to keep track of it all…

I work at a college which switched retirement plans but allowed me to leave my older 403(b) contributions with the previous company. I have a bank account, IRA, and a brokerage account. I also have a mortgage, gas and electric bills, various credit cards, cell phones, etc. All told I have about 20 accounts to keep track of.

Many people advise to combine as many accounts as possible, but if you are disciplined and can keep track of it all, some accounts have different options and some credit cards offer different services, so arguments can be made for keeping various options open. If you do not want to consolidate for whatever reason, you are left with the need to get organized.

How can one easily keep track of 20+ accounts? Check out yodlee.com Some banks offer Yodlee’s tools through their sites if you have an account with them so you may have seen this before. This service has been around and been free for a while- if you go directly to yodlee.com.

This service allows you to enter each account and enter your account name and password . Then when you log in to your Yodlee account, Yodlee logs in to each of your other accounts using your information and pulls the details together into one page.

To use a service like this you have to ask how much you trust Yodlee’s security processes and how valuable you find the consolidation. Personally, I love it. Once a month I log on, see my bills, add up how much I own, click on the button to log on to each credit card and the mortgage- Yodlee logs me on automatically without me needing to remember the account name for each site. I pay each bill and I can see if I have any extra money left over to move into my brokerageaccount and invest (not likely this time of year!).

I can see my total retirement savings, my non-retirement savings, my debt, etc. You can add any additional amount- even if you have an account that is not supported by Yodlee. For example, if you own a home, you can go to zillow.com, get an estimate on your home and enter the value as an account. If you have entered your mortgage, it will display your monthly statement as well as your total debt. Looking at your home's value next to its estimated worth you can how much equity you have built in your home.

Sure you can paste all of this into excel, or buy some financial software to help manage this, but Yodlee is free, makes paying bills and transferring funds a snap, and gives a quick snapshot of all your accounts without any maintenance.

Many people advise to combine as many accounts as possible, but if you are disciplined and can keep track of it all, some accounts have different options and some credit cards offer different services, so arguments can be made for keeping various options open. If you do not want to consolidate for whatever reason, you are left with the need to get organized.

How can one easily keep track of 20+ accounts? Check out yodlee.com Some banks offer Yodlee’s tools through their sites if you have an account with them so you may have seen this before. This service has been around and been free for a while- if you go directly to yodlee.com.

This service allows you to enter each account and enter your account name and password . Then when you log in to your Yodlee account, Yodlee logs in to each of your other accounts using your information and pulls the details together into one page.

To use a service like this you have to ask how much you trust Yodlee’s security processes and how valuable you find the consolidation. Personally, I love it. Once a month I log on, see my bills, add up how much I own, click on the button to log on to each credit card and the mortgage- Yodlee logs me on automatically without me needing to remember the account name for each site. I pay each bill and I can see if I have any extra money left over to move into my brokerageaccount and invest (not likely this time of year!).

I can see my total retirement savings, my non-retirement savings, my debt, etc. You can add any additional amount- even if you have an account that is not supported by Yodlee. For example, if you own a home, you can go to zillow.com, get an estimate on your home and enter the value as an account. If you have entered your mortgage, it will display your monthly statement as well as your total debt. Looking at your home's value next to its estimated worth you can how much equity you have built in your home.

Sure you can paste all of this into excel, or buy some financial software to help manage this, but Yodlee is free, makes paying bills and transferring funds a snap, and gives a quick snapshot of all your accounts without any maintenance.

Non-Ret: Small Cap Value

My Pick: STSCX Stratton Small Cap Value Fund

So far our hypothetical portfolio has a Mid Cap and a Large Cap fund but no Small Cap coverage and we have a Blend and a Growth fund but no Value so the next pick is Small Cap Value.

For this pick I tried to streamline the process of gathering the data I evaluate. Using Etrades’s Mutual Fund Screener, I selected Small Cap Value Funds and sorted by 5 year performance and cut and paste the data for the best 15 or so funds into a spreadsheet. Then I looked up the Expense info and cut and paste that into the spreadsheet. Then I looked up the profile info and copied that in.

Then I sorted by 3 year performance and did the same thing for the best 15 or so funds. Then I sorted by 1 year performance and copied the same info.

Then I sorted by Expenses and by Fund.

The first thing I noticed was that there was only one fund that was in the top funds for all three periods of time: Delafield Fund DEFIX. This was a tempting choice as consistency is key. There are three reasons I am not picking this fund. 1) Its turnover at 71% is above the average for this category which is 64.51%. 2) The initial purchase minimum is $5000 and I am trying to pick funds with $2500 initial minimum or lower. 3) This fund has shifted into Small Cap Value from Mid Cap Value so some of its performance came from moving from one category of companies to another. We will pick a Mid Cap Value fund and the Mid Cap Blend fund we already picked has coverage of the Value companies in this size so I do not want a Small cap fund that could drift back into Mid sized companies. None of these reasons are deal breakers necessarily so this fund would be a decent choice but I kept looking.

Kinetics Small Cap Opportunity Fund KSCOX was another fund I had to look at despite some red flags. It has done well since its inception and recently it has significantly outperformed its peers. It has higher than average expenses at 1.66% (the average is 1.36%) and higher than average turnover at 96%. There are a couple of other options that have also outperformed recently and have lower expenses and lower turnover so I kept looking.

I ruled out funds with above average expenses and then resorted and ruled out funds with above average turnover. Of the remaining funds there were four that stood out for various reasons:

STSCX has the highest 5 year and 3 year returns of the funds that have below average Expenses (1.28%) and Turnover and has the lowest turnover (15%) of these, but it has lagged its peers recently.

ICSCX has solid and consistent results and the lowest Expenses (0.87%) and very near the lowest Turnover (17%).

HRTVX has the highest 1 year results and has seriously outpaced STSCX and ICSCX over this period with below average Expenses (1.19%) and Turnover (36%).

ATASX has the highest year to date results but also has the highest Expenses (1.30%) and Turnover (56%) of these four.

All four funds have had consistent management over this period so I looked to see the minimum investment limits and if they have consistently invested in small cap value stocks.

STSCX has been consistent and has a $2000 initial minimum.

HRTVX has also been consistent but has a $5000 initial minimum which is too high for this portfolio.

ATASX has a $2500 minimum but has swung to Small Cap Growth and back.

ICSCX is closed to new investors.

ATASX has seriously outperformed STSCX recently, but over a 3 year period, STSCX has outperformed ATASX. The average price to earnings ratio of the stocks in STSCX is 18.52. The PE ratio of ATASX is 24.83 which is above the average for this group (19.60). Since I am looking for a value fund and the stocks in STSCX are cheaper (lower PE ratio), the expenses are less, the turnover is less, the consistency is better, I am not chasing short term performance and am choosing STSCX.

Next Category will be Foreign Small/Mid Cap Growth.

So far our hypothetical portfolio has a Mid Cap and a Large Cap fund but no Small Cap coverage and we have a Blend and a Growth fund but no Value so the next pick is Small Cap Value.

For this pick I tried to streamline the process of gathering the data I evaluate. Using Etrades’s Mutual Fund Screener, I selected Small Cap Value Funds and sorted by 5 year performance and cut and paste the data for the best 15 or so funds into a spreadsheet. Then I looked up the Expense info and cut and paste that into the spreadsheet. Then I looked up the profile info and copied that in.

Then I sorted by 3 year performance and did the same thing for the best 15 or so funds. Then I sorted by 1 year performance and copied the same info.

Then I sorted by Expenses and by Fund.

The first thing I noticed was that there was only one fund that was in the top funds for all three periods of time: Delafield Fund DEFIX. This was a tempting choice as consistency is key. There are three reasons I am not picking this fund. 1) Its turnover at 71% is above the average for this category which is 64.51%. 2) The initial purchase minimum is $5000 and I am trying to pick funds with $2500 initial minimum or lower. 3) This fund has shifted into Small Cap Value from Mid Cap Value so some of its performance came from moving from one category of companies to another. We will pick a Mid Cap Value fund and the Mid Cap Blend fund we already picked has coverage of the Value companies in this size so I do not want a Small cap fund that could drift back into Mid sized companies. None of these reasons are deal breakers necessarily so this fund would be a decent choice but I kept looking.

Kinetics Small Cap Opportunity Fund KSCOX was another fund I had to look at despite some red flags. It has done well since its inception and recently it has significantly outperformed its peers. It has higher than average expenses at 1.66% (the average is 1.36%) and higher than average turnover at 96%. There are a couple of other options that have also outperformed recently and have lower expenses and lower turnover so I kept looking.

I ruled out funds with above average expenses and then resorted and ruled out funds with above average turnover. Of the remaining funds there were four that stood out for various reasons:

STSCX has the highest 5 year and 3 year returns of the funds that have below average Expenses (1.28%) and Turnover and has the lowest turnover (15%) of these, but it has lagged its peers recently.

ICSCX has solid and consistent results and the lowest Expenses (0.87%) and very near the lowest Turnover (17%).

HRTVX has the highest 1 year results and has seriously outpaced STSCX and ICSCX over this period with below average Expenses (1.19%) and Turnover (36%).

ATASX has the highest year to date results but also has the highest Expenses (1.30%) and Turnover (56%) of these four.

All four funds have had consistent management over this period so I looked to see the minimum investment limits and if they have consistently invested in small cap value stocks.

STSCX has been consistent and has a $2000 initial minimum.

HRTVX has also been consistent but has a $5000 initial minimum which is too high for this portfolio.

ATASX has a $2500 minimum but has swung to Small Cap Growth and back.

ICSCX is closed to new investors.

ATASX has seriously outperformed STSCX recently, but over a 3 year period, STSCX has outperformed ATASX. The average price to earnings ratio of the stocks in STSCX is 18.52. The PE ratio of ATASX is 24.83 which is above the average for this group (19.60). Since I am looking for a value fund and the stocks in STSCX are cheaper (lower PE ratio), the expenses are less, the turnover is less, the consistency is better, I am not chasing short term performance and am choosing STSCX.

Next Category will be Foreign Small/Mid Cap Growth.

12.05.2006

Capital Gains Distributions Attack!

So December 4th was a good day for investors as the DOW, NASDAQ and S&P 500 were all up over +0.70%.

Two funds caught my eye yesterday as they posted serious declines in value (images from cnn.com):

PCOAX Putnam Capital Opportunities;A

PGRWX Putnam Growth & Income;A

So what gives? Many mutual funds make capital gains distributions. Often this is a result of portfolio turnover. Wikipeda explains it like this:

"Turnover generally has tax consequences for a fund, which are passed through to investors. In particular, when selling an investment from its portfolio, a fund may realize a capital gain, which will ultimately be distributed to investors as taxable income."

Someone holding the funds above would not see the total value of their holdings go down by 10% or 11%, assuming they were reinvesting their dividends and capital gains distributions, as the amount of the distribution would buy additional (now cheaper) shares of the fund.

Where this shows up is in the new year, when it comes times to pay taxes. The 10% that was distributed will show up on Form 1099-DIV from your brokerage as a taxable event. So you will owe taxes on the amount distributed.

One way to avoid or lessen the amount of capital gains distributions you receive is to invest in funds that do not sell the stocks they own very frequently- funds with lower turnover. In retirement accounts, IRAs 401(k)s or 403(b)s for example, your holds are not subject to taxes while they are held in the account so you do not pay taxes on these distributions. Kep in mind though that when a fund manager sells a stock, she pays a fee to do so, just like you would, and those fees are also passed on to shareholders so low turnover is good for a variety of reasons, even in tax free or tax deferred accounts.

That said, you will find that different strategies are used in categories- some categories have higher average turnover than others. The key here is not to pick the lowest turnover possible- if the fund is underperforming its peers for example. A better strategy is to pick a well performing fund with a lower than average turnover.

The Putnam Capital Opportunities fund Is a Small Cap Growth fund with 60.27% turnover. This is high, but the average for this category is 110.43% so this is below average. The bigger concern here is the 5.25% sales load. If you bought this fund at the beginning of the year and sold it on October 31st, you might be pleased with your anticipated windfall as the fund was up 13.09% at that point. The average gain for funds in this category was only 7.16%. However, after paying the 5.25% sales load, accounting for 1.20% in expenses and after paying taxes on profit and capital gains, the estimated take home here is 4.65%.

The Putnam Growth and Income fund is a different story with some similar issues. The first issue here is that, despite the name, this fund falls in the Large Cap Value category not the Large Cap Growth category. Funds do drift around and switch categories from time to time, but this fund has been solidly Value for a while:

Why does this matter? You should know what you have. Different sectors go in and out of favor. A lot of analysts think Large growth stocks are due for a run. If you owned this fund, you might think you have your investments poised to take advantage of this trend if it happens. You would be wrong and Putnam should be ashamed for misleading you or better yet, update the name of the fund. Anyway...

The average turnover for Large Cap Value funds is 55.91% and the average for Large Cap Growth is 83.76%. Since this fund is invested in Value stocks its turnover at 52.80% is... average. If you bought this at the beginning of the year and sold it at the end of Oct. you would not walk away with a 10.99% increase- you would take home around 3.34%.

When we choose a Large Cap Value fund for out hypothetical non-retirement account, we'll see if we can find a fund with lower turnover, and hopefully now it is a little more clear why we care!

Two funds caught my eye yesterday as they posted serious declines in value (images from cnn.com):

PCOAX Putnam Capital Opportunities;A

PGRWX Putnam Growth & Income;A

So what gives? Many mutual funds make capital gains distributions. Often this is a result of portfolio turnover. Wikipeda explains it like this:

"Turnover generally has tax consequences for a fund, which are passed through to investors. In particular, when selling an investment from its portfolio, a fund may realize a capital gain, which will ultimately be distributed to investors as taxable income."

Someone holding the funds above would not see the total value of their holdings go down by 10% or 11%, assuming they were reinvesting their dividends and capital gains distributions, as the amount of the distribution would buy additional (now cheaper) shares of the fund.

Where this shows up is in the new year, when it comes times to pay taxes. The 10% that was distributed will show up on Form 1099-DIV from your brokerage as a taxable event. So you will owe taxes on the amount distributed.

One way to avoid or lessen the amount of capital gains distributions you receive is to invest in funds that do not sell the stocks they own very frequently- funds with lower turnover. In retirement accounts, IRAs 401(k)s or 403(b)s for example, your holds are not subject to taxes while they are held in the account so you do not pay taxes on these distributions. Kep in mind though that when a fund manager sells a stock, she pays a fee to do so, just like you would, and those fees are also passed on to shareholders so low turnover is good for a variety of reasons, even in tax free or tax deferred accounts.

That said, you will find that different strategies are used in categories- some categories have higher average turnover than others. The key here is not to pick the lowest turnover possible- if the fund is underperforming its peers for example. A better strategy is to pick a well performing fund with a lower than average turnover.

The Putnam Capital Opportunities fund Is a Small Cap Growth fund with 60.27% turnover. This is high, but the average for this category is 110.43% so this is below average. The bigger concern here is the 5.25% sales load. If you bought this fund at the beginning of the year and sold it on October 31st, you might be pleased with your anticipated windfall as the fund was up 13.09% at that point. The average gain for funds in this category was only 7.16%. However, after paying the 5.25% sales load, accounting for 1.20% in expenses and after paying taxes on profit and capital gains, the estimated take home here is 4.65%.

The Putnam Growth and Income fund is a different story with some similar issues. The first issue here is that, despite the name, this fund falls in the Large Cap Value category not the Large Cap Growth category. Funds do drift around and switch categories from time to time, but this fund has been solidly Value for a while:

Why does this matter? You should know what you have. Different sectors go in and out of favor. A lot of analysts think Large growth stocks are due for a run. If you owned this fund, you might think you have your investments poised to take advantage of this trend if it happens. You would be wrong and Putnam should be ashamed for misleading you or better yet, update the name of the fund. Anyway...

The average turnover for Large Cap Value funds is 55.91% and the average for Large Cap Growth is 83.76%. Since this fund is invested in Value stocks its turnover at 52.80% is... average. If you bought this at the beginning of the year and sold it at the end of Oct. you would not walk away with a 10.99% increase- you would take home around 3.34%.

When we choose a Large Cap Value fund for out hypothetical non-retirement account, we'll see if we can find a fund with lower turnover, and hopefully now it is a little more clear why we care!

12.04.2006

I registered this site on Technorati.

I am not sure when you will be able to search for my posts at Technorati.com, here but I 'll keep an eye on it.

12.03.2006

Non-Ret: Large Cap Growth

My pick: JAGIX Janus Growth and Income Fund

Some of my first picks have been less popular categories, but searching for a Large Cap Growth fund, I found 96 options with no loads and no transaction costs available through etrade.

First, I sorted the options by 3 year performance. Then I looked at expenses and turnover. The average expenses for this category run 1.37% and the average turnover is 83.76%. Since I had so many choices, I was able to find options with lower expenses and turnover among the best performers when I went through the first 15 funds listed. During my first look at these I ruled out several funds including any with expenses over 1.20%:

JAMES EQUITY (JALCX) and JANUS ADVISER GROWTH & INCOME S (JADGX) are too expensive with 1.50% and 1.22% expense ratios respectively.

FIDELITY ADVISOR NEW INSIGHTS INSTL (FINSX) and JANUS TWENTY (JAVLX) are closed to new investors.

MARSICO 21ST CENTURY (MXXIX) has way too much turnover at 175% for a taxable account and is too expensive with a 1.39% expense ratio.

GENERATION WAVE GROWTH (GWGFX) 1.50% expense ratio is too high.

WELLS FARGO ADVTG CAPITAL GROWTH INV (SLGIX) is too expensive at 1.42%.

TURNER CORE GROWTH I (TTMEX) has very low 0.59% expenses but too much turnover at 136%.

Six of the first 15 funds are worth considering:

JANUS ADVISER FORTY S (JARTX) has a 1.18% expense ratio which is higher than some of the others but not too high.

TRANSAMERICA PREMIER EQUITY INV (TEQUX) looks interesting with a below average 1.09% expense ratio and 32%turnover rate.

EXCELSIOR LARGE CAP GROWTH (UMLGX) has below average expenses at 1.10% and has a low 24% turnover.

JANUS GROWTH & INCOME (JAGIX) has very low expenses at 0.87% and below average 38% turnover.

WESTCORE BLUE CHIP (WTMVX) has 1.11% expenses and 50% turnover

SIT LARGE CAP GROWTH (SNIGX) has low 1.00% expense ratio and 24% turnover.

T ROWE PRICE GROWTH STOCK ADV (TRSAX) has low expenses at 0.94% and 36% turnover.

Looming at these six funds, the performance of some has been better recently some better over the long term. Chasing near term performance is never a good idea, so I sort by lowest expenses:

TRSAX has performed better than JAGIX recently, but JAGIX has a better 3 year performance record. Either fund would work. TRSAX looks like it tracks Large cap domestic indexes more closely. JAGIX has a Large Cap Domestic base but also holds international funds and some stock in smaller companies. Janus is known for being a more aggressive fund company in general. This hurt investors who bought Janus funds at the peak of the market in 2000. But for the purposes of this hypothetical portfolio- with a plan to invest regularly, a more aggressive fund, with lower expenses, is my choice.

Some of my first picks have been less popular categories, but searching for a Large Cap Growth fund, I found 96 options with no loads and no transaction costs available through etrade.

First, I sorted the options by 3 year performance. Then I looked at expenses and turnover. The average expenses for this category run 1.37% and the average turnover is 83.76%. Since I had so many choices, I was able to find options with lower expenses and turnover among the best performers when I went through the first 15 funds listed. During my first look at these I ruled out several funds including any with expenses over 1.20%:

JAMES EQUITY (JALCX) and JANUS ADVISER GROWTH & INCOME S (JADGX) are too expensive with 1.50% and 1.22% expense ratios respectively.

FIDELITY ADVISOR NEW INSIGHTS INSTL (FINSX) and JANUS TWENTY (JAVLX) are closed to new investors.

MARSICO 21ST CENTURY (MXXIX) has way too much turnover at 175% for a taxable account and is too expensive with a 1.39% expense ratio.

GENERATION WAVE GROWTH (GWGFX) 1.50% expense ratio is too high.

WELLS FARGO ADVTG CAPITAL GROWTH INV (SLGIX) is too expensive at 1.42%.

TURNER CORE GROWTH I (TTMEX) has very low 0.59% expenses but too much turnover at 136%.

Six of the first 15 funds are worth considering:

JANUS ADVISER FORTY S (JARTX) has a 1.18% expense ratio which is higher than some of the others but not too high.

TRANSAMERICA PREMIER EQUITY INV (TEQUX) looks interesting with a below average 1.09% expense ratio and 32%turnover rate.

EXCELSIOR LARGE CAP GROWTH (UMLGX) has below average expenses at 1.10% and has a low 24% turnover.

JANUS GROWTH & INCOME (JAGIX) has very low expenses at 0.87% and below average 38% turnover.

WESTCORE BLUE CHIP (WTMVX) has 1.11% expenses and 50% turnover

SIT LARGE CAP GROWTH (SNIGX) has low 1.00% expense ratio and 24% turnover.

T ROWE PRICE GROWTH STOCK ADV (TRSAX) has low expenses at 0.94% and 36% turnover.

Looming at these six funds, the performance of some has been better recently some better over the long term. Chasing near term performance is never a good idea, so I sort by lowest expenses:

TRSAX has performed better than JAGIX recently, but JAGIX has a better 3 year performance record. Either fund would work. TRSAX looks like it tracks Large cap domestic indexes more closely. JAGIX has a Large Cap Domestic base but also holds international funds and some stock in smaller companies. Janus is known for being a more aggressive fund company in general. This hurt investors who bought Janus funds at the peak of the market in 2000. But for the purposes of this hypothetical portfolio- with a plan to invest regularly, a more aggressive fund, with lower expenses, is my choice.

11.26.2006

What is a fund category?

Wells Fargo has a page that goes into some detail about what a fund category means and the risks typically associated with each category.

I think Wells Fargo's page is much clearer than Morningstar's own explanations. Maybe Morningstar has a better page somewhere, but I don't see it...

I think Wells Fargo's page is much clearer than Morningstar's own explanations. Maybe Morningstar has a better page somewhere, but I don't see it...

Non-Ret: Bond Gov. Long

My Pick: BTTRX American Century Target Maturity 2025/Inv

The first two funds picked, Mid Cap Blend and Global Equity, might be deemed by some as riskier than the typical stock pick. To further diversify, and hopefully offset some of the risk, the next fund I will add to this hypothetical portfolio will be a bond fund. By picking Government bonds, credit risks are reduced. Besides, if the US defaults on its debt, we will likely have more pressing concerns than the performance of this particular fund. Also, since we added a solid international funds, as money pours out US securities, it should poor into the Global fund we picked. Well, it might. Anyway, bonds with longer duration tend to react more to changes in interest rates, so this is not the least risky bond fund category.

So, I pull up no-load, no fees and sort by 3 year performance. BTTRX comes up as the top performer by a good margin over 10, 5 and 3 year ranges. It has slightly underperformed BTTTX over the last year and is actually down slightly for the year, but not by much and BTTTX is only up 0.83%.

There are no other funds in this category that I like. The one downside to these funds is that the minimum initial investment is $2500, compared to $1000 for each of our first two picks. So I checked and all the other funds in this category that have performed decently have a $2500 initial investment or higher

Expenses are the exact same, but BTTRX has a 26% turnover rate compared to BTTTX at 10%. Both funds are managed by the same manager and team (Jeremy Fletcher).

Either option would work as expenses, turnover, performance are all relatively close. In this case, I am choosing the fund with the better long term performance record: BTTRX. Searching for all funds available in this category through Etrade, these are still the best options, so even if you are not looking to contribute additional small amounts, these are worth considering if you are looking for a Long Term Government Bond mutual fund.

The first two funds picked, Mid Cap Blend and Global Equity, might be deemed by some as riskier than the typical stock pick. To further diversify, and hopefully offset some of the risk, the next fund I will add to this hypothetical portfolio will be a bond fund. By picking Government bonds, credit risks are reduced. Besides, if the US defaults on its debt, we will likely have more pressing concerns than the performance of this particular fund. Also, since we added a solid international funds, as money pours out US securities, it should poor into the Global fund we picked. Well, it might. Anyway, bonds with longer duration tend to react more to changes in interest rates, so this is not the least risky bond fund category.

So, I pull up no-load, no fees and sort by 3 year performance. BTTRX comes up as the top performer by a good margin over 10, 5 and 3 year ranges. It has slightly underperformed BTTTX over the last year and is actually down slightly for the year, but not by much and BTTTX is only up 0.83%.

There are no other funds in this category that I like. The one downside to these funds is that the minimum initial investment is $2500, compared to $1000 for each of our first two picks. So I checked and all the other funds in this category that have performed decently have a $2500 initial investment or higher

Expenses are the exact same, but BTTRX has a 26% turnover rate compared to BTTTX at 10%. Both funds are managed by the same manager and team (Jeremy Fletcher).

Either option would work as expenses, turnover, performance are all relatively close. In this case, I am choosing the fund with the better long term performance record: BTTRX. Searching for all funds available in this category through Etrade, these are still the best options, so even if you are not looking to contribute additional small amounts, these are worth considering if you are looking for a Long Term Government Bond mutual fund.

11.22.2006

11.20.2006

Non-Ret: Global Equity

My pick: MDISX Mutual Discovery Fund/Z

The next recommendation for this hypothetical non-retirement account is a Global Equity fund or World Stock. This is an international fund that has a large US component and generally also invests some in emerging markets.

Since I am building a portfolio that could be built in this specific order, I picked a blend category first and this broad category second. I think international exposure is good for diversifying, but owning only an emerging markets fund or specific overseas category along with only a domestic Mid Cap Blend, would be pretty narrow, so World Stock it is.

The average turnover for funds in this category is 58.25% and the average expense ratio is 1.45%. Searching through the offerings and looking at the criteria I care about, I find 5 that look promising but quickly note that 2 are closed to new investors (OAKGX, SCOBX). A third (BJGQX) has $1000 minimum for subsequent investments and an above average expense ratio so despite a good track record, I rule it out.

That leaves only two options, but they are among the top performers, have $100 minimum for subsequent investments and lower than average turnover and expenses. MDISX Mutual Discovery Fund/Z and JSVAX Janus Contrarian Fund have both performed really well over the last 5 years, 3 years, 1 year and YTD. This is good reason to pause and wonder if these funds are not due to slow down or pull back. Since our proposed portfolio will invest over time, we have reduced the risk a down-turn poses and the average Price to earning ratio of stocks held in these funds is not too high (13.4 for MDISX and 17.5 for JSVAX according to Morningstar) so the holdings do not seem overpriced, on average.

Here is a breakdown:

Portfolio Turnover (Average 58.25%)

*MDISX 25.69%

JSVAX 42.00%

Expense Ratio (Average 1.45%)

MDISX 1.04%

*JSVAX 0.93%

Performance

So MDISX has much lower turnover which could help keep capital gains tax low. It has a slightly higher expense ratio, but only by 0.11% It has performed about the same, but slightly better recently than JSVAX. For those reasons and because I anticipate I will pick some Janus funds when looking at Domestic Growth stocks, and I want to pick from different fund companies if I find good options, my pick here is MDISX.

The next recommendation for this hypothetical non-retirement account is a Global Equity fund or World Stock. This is an international fund that has a large US component and generally also invests some in emerging markets.

Since I am building a portfolio that could be built in this specific order, I picked a blend category first and this broad category second. I think international exposure is good for diversifying, but owning only an emerging markets fund or specific overseas category along with only a domestic Mid Cap Blend, would be pretty narrow, so World Stock it is.

The average turnover for funds in this category is 58.25% and the average expense ratio is 1.45%. Searching through the offerings and looking at the criteria I care about, I find 5 that look promising but quickly note that 2 are closed to new investors (OAKGX, SCOBX). A third (BJGQX) has $1000 minimum for subsequent investments and an above average expense ratio so despite a good track record, I rule it out.

That leaves only two options, but they are among the top performers, have $100 minimum for subsequent investments and lower than average turnover and expenses. MDISX Mutual Discovery Fund/Z and JSVAX Janus Contrarian Fund have both performed really well over the last 5 years, 3 years, 1 year and YTD. This is good reason to pause and wonder if these funds are not due to slow down or pull back. Since our proposed portfolio will invest over time, we have reduced the risk a down-turn poses and the average Price to earning ratio of stocks held in these funds is not too high (13.4 for MDISX and 17.5 for JSVAX according to Morningstar) so the holdings do not seem overpriced, on average.

Here is a breakdown:

Portfolio Turnover (Average 58.25%)

*MDISX 25.69%

JSVAX 42.00%

Expense Ratio (Average 1.45%)

MDISX 1.04%

*JSVAX 0.93%

Performance

So MDISX has much lower turnover which could help keep capital gains tax low. It has a slightly higher expense ratio, but only by 0.11% It has performed about the same, but slightly better recently than JSVAX. For those reasons and because I anticipate I will pick some Janus funds when looking at Domestic Growth stocks, and I want to pick from different fund companies if I find good options, my pick here is MDISX.

11.14.2006

Etrade: Mutual fund offerings

I would avoid using a brokerage that only offers funds of one company. Putnam, Janus, Fidelity etc. To better diversify, it is important to pick funds from different companies as well as from different sectors. Even though funds at one company may have different managers and focus on different market sectors, sometimes they use the same pool of analysts so funds covering ‘different’ market sectors may end up holding the same companies resulting in a less diverse portfolio. Besides, I am not aware of one fund company that covers all the sectors I want to cover and also beats the averages of funds covering those sectors, in every case. If any of you know about one, let me know!

As mentioned before, I will use Etrade for this hypothetical portfolio, but other brokerage may offer the tools to set up a similar plan. Motley Fool's website has a comparison of a few brokerages and Dogs of the Dow's site offers more information including customer feedback.

Etrade offers funds from many families and most critical to the wealth building scheme I propose to develop, it offers many no-load funds available for purchase for no fee (It advertises over 1000 of these). One family of funds I like to keep an eye on that is not well represented at Etrade currently is Artisan.

A search for no-load, no-fee funds finds 1158, but some of these are closed to new investors and some have minimum initial investments of $1 million or more, so the actual number of open no-load no-fee funds with minimum investment amounts of say $5000 or less is not clear. It would be nice if the fund screener tool let you exclude funds with high minimum investments or that are closed to new investors, but it does not.

As mentioned before, I will use Etrade for this hypothetical portfolio, but other brokerage may offer the tools to set up a similar plan. Motley Fool's website has a comparison of a few brokerages and Dogs of the Dow's site offers more information including customer feedback.

Etrade offers funds from many families and most critical to the wealth building scheme I propose to develop, it offers many no-load funds available for purchase for no fee (It advertises over 1000 of these). One family of funds I like to keep an eye on that is not well represented at Etrade currently is Artisan.

A search for no-load, no-fee funds finds 1158, but some of these are closed to new investors and some have minimum initial investments of $1 million or more, so the actual number of open no-load no-fee funds with minimum investment amounts of say $5000 or less is not clear. It would be nice if the fund screener tool let you exclude funds with high minimum investments or that are closed to new investors, but it does not.

11.12.2006

Non-Ret: Mid Cap Blend

My pick: NTIAX Columbia Mid Cap Index Fund/A

Using the Mutual fund Screener to identify No-Load, No-Fee funds with a Style: ‘Equity Mid Cap Blend,’ I find 18 options. I start by finding the average turnover rate: 76.87% and expense ratio 1.20% of funds in this category. Then I look at the Funds sorted by best 5 year annual performance and look for funds with $3000 or lower initial purchase minimum and $100 subsequent investment minimum and turnover and expenses equal to or lower than the minimum. I will also check whether they are consistently investing in mid cap companies. All these details are as of 11/12/06.

The first funds listed have done well but I rule them out for these reasons:

UMPIX ProFunds: UltraMid Cap/Inv has a really high 402.00% portfolio turnover, and a $15,000 initial minimum purchase as well as a 1.49% expense ratio.

ASMCX Accessor Funds: Small to Mid Cap/Adv has a $1,000 minimum for subsequent investment. Also this fund splits between mid and small cap companies and following this plan, we will select a separate fund covering small cap companies.

RIMSX Rainier Investment: Sm/Md Cap Eqty Port has a $25,000 initial min, $1,000 Subsequent min. In addition, it has a significant portion of its holdings in small cap companies.

ACSIX Accessor Funds: Small to Mid Cap/Inv has a $5,000 initial min. which is a little higher than I want but $1,000 Subsequent min. is much too high. The 1.64% expense ration is also above average and again, some of the recent out-performance is due to investing in small cap companies which have done well recently.

The next three funds listed:

CHTTX ABN AMRO Mid Cap Fund/N has very low portfolio turnover 27.42%, average expense ratio of 1.23%, and $2,500 and $50 initial and subsequent minimums. This is a definite candidate.

PESPX Dreyfus Index Fds: Midcap Index Fund has $2,500 and $100 initial and subsequent minimums, a 0.50% Expense Ratio and a low 19.54% turnover rate. Another candidate.

NTIAX Columbia Mid Cap Index Fund/A has $1,000 and $100 initial and subsequent minimums, a 0.39 Expense Ratio and a low 24.00% turnover rate. A third candidate.

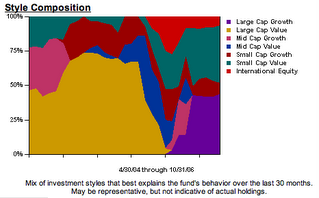

In looking at CHTTX, I immediatley notice that it is investing a great deal in stocks of companies other than mid cap domestic companies. As you can see by this graphic:

Basically there are no managed funds that meet the criteria for my portfolio in the Mid Cap Blend style, but there are 2 index funds that do. Either PESPX or NTIAX would be a good option- both have low turnover rates and low expenses, as you would expect with index funds. There is one big difference PESPX has 2,269.3 million under management compared to 37.7 million for NTIAX. This could explain why the expenses on NTIAX are a little bit lower. NTIAX has slightly lower expenses and has ever so slightly out-performed PESPX over the 3 year and one year periods, so I will go with NTIAX.

When looking at funds available through Etrade, a fund available for a transaction fee (meaning it would not be a candidate for investing additional $100 contributions over time) VIMSX Vanguard Mid Cap Index/Inv has an even lower 0.22% expense ratio, and a low 18.00% portfolio turnover. There are a few other funds that have performed a bit better than this index fund, but they have 1% or more higher annual expense ratios and are investing in many sectors other than domestic mid cap companies. In addition to being cheaper, VIMSX has outperformed NTIAX, so it is too bad that it is not available for no fee.

Using the Mutual fund Screener to identify No-Load, No-Fee funds with a Style: ‘Equity Mid Cap Blend,’ I find 18 options. I start by finding the average turnover rate: 76.87% and expense ratio 1.20% of funds in this category. Then I look at the Funds sorted by best 5 year annual performance and look for funds with $3000 or lower initial purchase minimum and $100 subsequent investment minimum and turnover and expenses equal to or lower than the minimum. I will also check whether they are consistently investing in mid cap companies. All these details are as of 11/12/06.

The first funds listed have done well but I rule them out for these reasons:

UMPIX ProFunds: UltraMid Cap/Inv has a really high 402.00% portfolio turnover, and a $15,000 initial minimum purchase as well as a 1.49% expense ratio.

ASMCX Accessor Funds: Small to Mid Cap/Adv has a $1,000 minimum for subsequent investment. Also this fund splits between mid and small cap companies and following this plan, we will select a separate fund covering small cap companies.

RIMSX Rainier Investment: Sm/Md Cap Eqty Port has a $25,000 initial min, $1,000 Subsequent min. In addition, it has a significant portion of its holdings in small cap companies.

ACSIX Accessor Funds: Small to Mid Cap/Inv has a $5,000 initial min. which is a little higher than I want but $1,000 Subsequent min. is much too high. The 1.64% expense ration is also above average and again, some of the recent out-performance is due to investing in small cap companies which have done well recently.

The next three funds listed:

CHTTX ABN AMRO Mid Cap Fund/N has very low portfolio turnover 27.42%, average expense ratio of 1.23%, and $2,500 and $50 initial and subsequent minimums. This is a definite candidate.

PESPX Dreyfus Index Fds: Midcap Index Fund has $2,500 and $100 initial and subsequent minimums, a 0.50% Expense Ratio and a low 19.54% turnover rate. Another candidate.

NTIAX Columbia Mid Cap Index Fund/A has $1,000 and $100 initial and subsequent minimums, a 0.39 Expense Ratio and a low 24.00% turnover rate. A third candidate.

In looking at CHTTX, I immediatley notice that it is investing a great deal in stocks of companies other than mid cap domestic companies. As you can see by this graphic:

Basically there are no managed funds that meet the criteria for my portfolio in the Mid Cap Blend style, but there are 2 index funds that do. Either PESPX or NTIAX would be a good option- both have low turnover rates and low expenses, as you would expect with index funds. There is one big difference PESPX has 2,269.3 million under management compared to 37.7 million for NTIAX. This could explain why the expenses on NTIAX are a little bit lower. NTIAX has slightly lower expenses and has ever so slightly out-performed PESPX over the 3 year and one year periods, so I will go with NTIAX.

When looking at funds available through Etrade, a fund available for a transaction fee (meaning it would not be a candidate for investing additional $100 contributions over time) VIMSX Vanguard Mid Cap Index/Inv has an even lower 0.22% expense ratio, and a low 18.00% portfolio turnover. There are a few other funds that have performed a bit better than this index fund, but they have 1% or more higher annual expense ratios and are investing in many sectors other than domestic mid cap companies. In addition to being cheaper, VIMSX has outperformed NTIAX, so it is too bad that it is not available for no fee.

11.10.2006

Etrade: Fees

The info on this post is from 11/10/06 and will change so do your own research if you are interested in finding out more, whenever you are ready. Also, these are the fees that will or could impact a plan like the one I am proposing, not a complete list of fees.

Minimum Balance Fee:

$40 quarterly Low Balance Fee -if the balance in your E*TRADE Securities account is over $10,000 or the total combined balance in your linked E*TRADE Securities and E*TRADE Bank accounts is over $20,000 you do not have to pay this. Also, these fees are not charged for accounts in the first year (this is a nasty policy) .

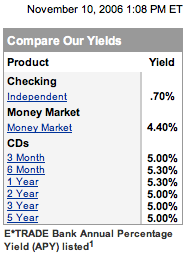

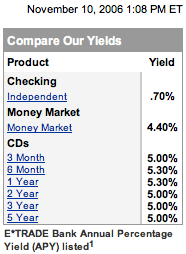

You should not set up a non-retirement brokerage account with Etrade unless you have more than $10,000 that will remain there until the account is closed as paying $160 annually in maintenance fees is ridiculous and you can easily find a different brokerage that does not charge this. Also, I do not recommend opening an Etrade bank account. All their adds suggest a savings rate of 4.4% which is not great but not bad especially compared to what many local branches offer.

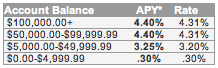

When you dig around, however, you will find that if your balance is under $5000, the current rate is .30%.

You can find an online bank account with better rates without balance restrictions. Bank Deals is an excellent site for tracking down online banks.

Minimum Balance Fee:

$40 quarterly Low Balance Fee -if the balance in your E*TRADE Securities account is over $10,000 or the total combined balance in your linked E*TRADE Securities and E*TRADE Bank accounts is over $20,000 you do not have to pay this. Also, these fees are not charged for accounts in the first year (this is a nasty policy) .

You should not set up a non-retirement brokerage account with Etrade unless you have more than $10,000 that will remain there until the account is closed as paying $160 annually in maintenance fees is ridiculous and you can easily find a different brokerage that does not charge this. Also, I do not recommend opening an Etrade bank account. All their adds suggest a savings rate of 4.4% which is not great but not bad especially compared to what many local branches offer.

When you dig around, however, you will find that if your balance is under $5000, the current rate is .30%.

You can find an online bank account with better rates without balance restrictions. Bank Deals is an excellent site for tracking down online banks.

11.08.2006

Brokerage Accounts: Thoughts about Etrade

I have an Etrade account and will limit my choices to funds available through Etrade, as long as I continue to use Etrade. Let me start by saying that I did not choose Etrade, but I am satisfied with it. I opened a Discover brokerage account which became a Morgan Stanley account which became a HarrisDirect account which then became an Etrade account. The things I keep an eye on are Fees, Mutual Fund offerings, Services and Tools, and Yields on cash held in the account. This can be a bit tedious since brokerages merge, get bought, and change fees and services constantly (see above), but unlike what the market does, you can control what fees you pay and what services you use by keeping abreast of what the competition is offering and change your brokerage if necessary. If you think about brokerages in this light, one of the most important things to identify before setting up an account is the “Account closing fee.”

Another point- The internet is overflowing with Etrade customer service complaints. I too have had difficult and tedious customer service experiences with Etrade, though like many- I was persistent and ultimately reached someone who helped me more than I thought they would. That said- I would be interested in hearing if other full service brokerages offer a broad range of no-load no-fee mutual funds and if other brokerages have better customer service. Such funds are also referred to as NTF (No Transaction Fee) Funds.

Before I start picking funds, I will look at Fees, Mutual Fund offerings, Services and Tools, and Yields on cash held in the account.

Another point- The internet is overflowing with Etrade customer service complaints. I too have had difficult and tedious customer service experiences with Etrade, though like many- I was persistent and ultimately reached someone who helped me more than I thought they would. That said- I would be interested in hearing if other full service brokerages offer a broad range of no-load no-fee mutual funds and if other brokerages have better customer service. Such funds are also referred to as NTF (No Transaction Fee) Funds.

Before I start picking funds, I will look at Fees, Mutual Fund offerings, Services and Tools, and Yields on cash held in the account.

11.07.2006

The Approach: Non-Retirement Portfolio

Let me start by indicating that this blend of stocks and (very few) bonds would be deemed “Extremely Aggressive” by most standards. While I think investing in a mix as diverse as this is actually less risky than investing in what many would consider a far less aggressive portfolio, I think it best to indicate that this is by no means meant to be strategy that does not run the risk of losing value. And continuing to add to a portfolio that is losing value month after month, as should happen at some point, will be trying, but should also garner better returns when the market trends upwards, as it should.

First I will identify market sectors I want to invest in. Large and Small companies, Growth and Value oriented businesses, International companies, Bonds, Real Estate Investment Trusts, etc. Then I will come up with an order in which I should add additional sectors to my portfolio to quickly diversify and then remain balanced as I increase the breadth of sectors I am invested in. I broke down portfolios based on the ability to invest monthly one of the following amounts: $300, $500, $1000, $1500, $2000, and $2500. I could certainly invest anywhere between $100 to $2500 but the placement of each sector at each point from 1 to 25 was intended to set up portfolios of 3, 5, 10, 15, 20, or 25 funds keeping each group loosely balanced.

For each sector I am going to research what no-load, no-fee funds are available to new investors in Etrade and which ones have $100 or less minimum for additional investments.. I am going to identify the top performing funds with a decent track record and then pick the fund with the lowest expenses and the lowest portfolio turnover. Turnover is critical because higher turnover can translate into higher annual tax bills, regardless of whether the performance is better or not. Since this is a non-retirement account, that can make a significant difference over the long term. I will also look at management tenure, average P/E ratios of stocks held within the fund, the initial amount required to purchase, etc.

I want to stress that I am not going to compare these factors in an extremely precise way. If the numbers of two funds are close, I am not going to follow a system and pick the one with a fraction of a percent lowers on one number or the other. I may choose a fund with higher expenses if the potential for performance seems greater (but it would have to be a lot greater to compensate for higher expenses over time) or if the turnover is lower, hoping the tax savings offset the expense difference. I will try and indicate the things I find in my research and the reasons I choose the funds I do.

First I will identify market sectors I want to invest in. Large and Small companies, Growth and Value oriented businesses, International companies, Bonds, Real Estate Investment Trusts, etc. Then I will come up with an order in which I should add additional sectors to my portfolio to quickly diversify and then remain balanced as I increase the breadth of sectors I am invested in. I broke down portfolios based on the ability to invest monthly one of the following amounts: $300, $500, $1000, $1500, $2000, and $2500. I could certainly invest anywhere between $100 to $2500 but the placement of each sector at each point from 1 to 25 was intended to set up portfolios of 3, 5, 10, 15, 20, or 25 funds keeping each group loosely balanced.

For each sector I am going to research what no-load, no-fee funds are available to new investors in Etrade and which ones have $100 or less minimum for additional investments.. I am going to identify the top performing funds with a decent track record and then pick the fund with the lowest expenses and the lowest portfolio turnover. Turnover is critical because higher turnover can translate into higher annual tax bills, regardless of whether the performance is better or not. Since this is a non-retirement account, that can make a significant difference over the long term. I will also look at management tenure, average P/E ratios of stocks held within the fund, the initial amount required to purchase, etc.

I want to stress that I am not going to compare these factors in an extremely precise way. If the numbers of two funds are close, I am not going to follow a system and pick the one with a fraction of a percent lowers on one number or the other. I may choose a fund with higher expenses if the potential for performance seems greater (but it would have to be a lot greater to compensate for higher expenses over time) or if the turnover is lower, hoping the tax savings offset the expense difference. I will try and indicate the things I find in my research and the reasons I choose the funds I do.

11.06.2006

The Plan: Non-Retirement Portfolio

What I am proposing is a plan for building a broadly diversified collection of mutual funds with automatic monthly investments in a non-retirement account. It is my hope that this is a good plan for me as someone with little to no credit card debt, reasonably stable income and living comfortably below my means. I also do not want to spend a great deal of time researching and staying on top of individual stocks and bonds. This is a plan for growing wealth, not generating additional income. It is a plan for long-term investing.

If I did not have the income to invest at least $300 per month- this would not be a good approach. I will be choosing funds that charge no fee to purchase. There are funds in every sector I will pick that would be better options if I had a fixed amount of money I wanted to invest in a specific fund all at once. I am limiting my choices to funds that will allow automatic investing because I believe that the discipline of contributing consistently will mean I invest more and the benefit of investing over time through market peaks and valleys will help reduce the negative impact of buying during a market peak.

Each mutual fund will have a minimum investment amount to initially purchase the fund and each fund I choose will have $100 or less additional investment minimum. This plan should work for me as long as I can add between $300 and $2500 per month (That is a big range, but I am serious about building wealth. It should work for me if my financial situation improves meaning if I can invest $300 per month now and can bump that up to $500 later, it should work well. It should be scalable. It should allow me to add additional funds slowly as I save the additional money needed to add each new fund.

If I could invest more than $2500 per month, but still do not want to get more active than this in managing my own investments, I would probably research and hire a good financial planner or advisor. Some will argue that I should do this anyway and some will argue that if I have over $500 I should do this. I am not recommending that you do anything. I hope to build a plan that will build a diversified portfolio of funds that should be a relatively low maintenance way to invest over the long term without stressing about timing the market.

If I did not have the income to invest at least $300 per month- this would not be a good approach. I will be choosing funds that charge no fee to purchase. There are funds in every sector I will pick that would be better options if I had a fixed amount of money I wanted to invest in a specific fund all at once. I am limiting my choices to funds that will allow automatic investing because I believe that the discipline of contributing consistently will mean I invest more and the benefit of investing over time through market peaks and valleys will help reduce the negative impact of buying during a market peak.

Each mutual fund will have a minimum investment amount to initially purchase the fund and each fund I choose will have $100 or less additional investment minimum. This plan should work for me as long as I can add between $300 and $2500 per month (That is a big range, but I am serious about building wealth. It should work for me if my financial situation improves meaning if I can invest $300 per month now and can bump that up to $500 later, it should work well. It should be scalable. It should allow me to add additional funds slowly as I save the additional money needed to add each new fund.

If I could invest more than $2500 per month, but still do not want to get more active than this in managing my own investments, I would probably research and hire a good financial planner or advisor. Some will argue that I should do this anyway and some will argue that if I have over $500 I should do this. I am not recommending that you do anything. I hope to build a plan that will build a diversified portfolio of funds that should be a relatively low maintenance way to invest over the long term without stressing about timing the market.

Subscribe to:

Posts (Atom)